It's optional to accept health insurance through your employer. You can deny or waive this benefit and get health insurance on your own.

Written by Erik Martin

Erik Martin

Erik J. Martin is a Chicago area-based freelance writer whose articles have been published by AARP The Magazine, The Motley Fool, The Costco Connection, USAA, US Chamber of Commerce, Bankrate, The Chicago Tribune, and other publications. He often writes on topics related to insurance, real estate, personal finance, business, technology, health care, and entertainment. Erik also hosts a podcast and publishes several blogs, including Martinspiration.com and Cineversegroup.com.

Reviewed by John McCormick

John McCormick

John is the editorial director for CarInsurance.com, Insurance.com and Insure.com. Before joining QuinStreet, John was a deputy editor at The Wall Street Journal and had been an editor and reporter at a number of other media outlets where he covered insurance, personal finance, and technology.

Updated on : February 21, 2024Why you can trust Insure.com

At Insure.com, we are committed to providing the timely, accurate and expert information consumers need to make smart insurance decisions. All our content is written and reviewed by industry professionals and insurance experts. Our team carefully vets our rate data to ensure we only provide reliable and up-to-date insurance pricing. We follow the highest editorial standards. Our content is based solely on objective research and data gathering. We maintain strict editorial independence to ensure unbiased coverage of the insurance industry.

Employer-sponsored health insurance plans are often more affordable than seeking coverage on your own. But if you need to, you can still decline coverage. Although some restrictions apply, you aren’t required to accept your company’s health insurance coverage.

It may make more sense to decline employer health insurance and opt for a plan through the Healthcare.gov marketplace, directly from a private health insurance company, or through another source, such as Medicare or Medicaid. Some people also get coverage under their spouse’s plan.

Read on to learn more about the advantages and disadvantages of employer-sponsored health insurance.

Employer-sponsored health insurance is optional. In most cases, employers typically offer health insurance as part of their benefits package, but they usually don’t require employees to enroll in it.

In many places, employees can either accept or decline the health insurance coverage provided by their employer. Some employers may have a policy encouraging or requiring employees to participate in the company-sponsored health insurance plan, but this varies.

Employer-sponsored health insurance is often more affordable than an individual plan, but not always — and you may find an ACA plan with a better provider network.

Brian Colburn, senior vice president of corporate development & strategy at Waltham, Massachusetts-headquartered Alegeus, says that, despite the advantages of employer group insurance plans, many still choose to purchase individual health insurance.

“Often, this happens when the employee’s needs don’t match what the employer-sponsored coverage offers. If you have unique healthcare needs, desire doctors and specialists out of network, or want a more bare-bones plan, the individual marketplace can be a good alternative,” says Colburn.

Neat explains that shopping for coverage at Healthcare.gov may be best if you qualify for an income-based subsidy. The ACA marketplace provides subsidies and tax credits to help people pay for ACA plans. The subsidies can save members hundreds of dollars each month, but they aren’t available for plans outside the ACA marketplace.

“If you are self-employed or do not have affordable options at work, an individual ACA or private marketplace plan may be the only option in your area. The good news is that ACA plans have no penalties for pre-existing conditions, so if you are struggling with a health condition, this may be your best choice,” she says.

You aren’t required to accept an employer health insurance plan. You can decline or waive this benefit and get your own insurance.

“But you may have to sign a waiver that you will be obtaining another insurance plan or accepting someone else’s insurance coverage so that your employer has proof that you are insured for legal purposes,” Schrader says.

If you decline or waive your employer-sponsored coverage, you can enroll later during the employer’s open enrollment period unless you qualify for a special enrollment because of a qualifying event.

“Certain qualifying life events, such as you losing coverage not provided by your employer, getting married or having children may trigger a special open enrollment period during which you can sign up for group coverage at work, too,” says Kronk.

Also, after signing up for employer-sponsored health coverage and agreeing to deduct your premiums from your paychecks, “you can’t drop coverage during the year unless you experience a qualifying life event,” says Colburn.

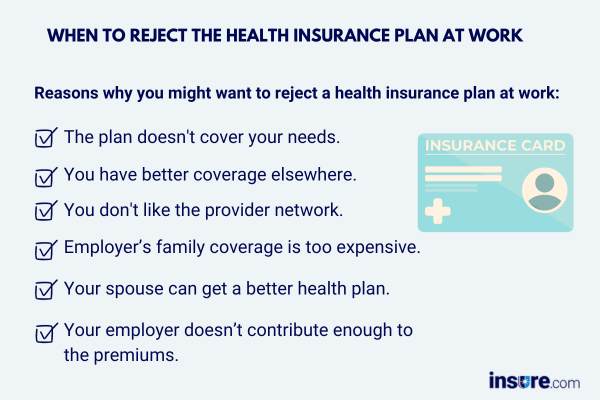

Here are some of the scenarios when you might want to opt out of group insurance at work and buy health insurance on your own.

For employer-sponsored coverage, employers decide on the health insurance company, network, copays and deductibles. This health coverage is only provided to those currently employed and their dependents and isn’t individualized.

However, people may find coverage for individuals and families through the ACA exchange or directly from insurance companies that better fit their needs. That way, they can choose the copays, out-of-pocket costs and benefits that make sense to them, such as a health maintenance organization (HMO) or preferred provider organization (PPO)

Here is how an employer-sponsored plan compares to other health coverage options:

| Plan | Pros | Cons |

|---|---|---|

| Employer-sponsored health insurance | Employer helps pay so it can be more affordable than other options You can usually add your spouse and dependents to the plan | Limited to your employer’s choices Coverage is limited to your employment, so if you lose your job, you can get COBRA, which is expensive, or you have to find another plan |

| ACA plan through the marketplace | ACA marketplace offers multiple options in most parts of the country Gives you more flexibility to find a health plan that may fit your needs If you qualify for subsidies, you may find a plan more affordable than an employer plan | Without subsidies, ACA plans can be pricey Most areas have multiple ACA plans of varying benefit design and costs Some parts of the country have limited options ACA plans often have limited provider networks |

| Individual plan outside the marketplace | More choices, but takes some digging to see which plans are offered in your area You’re not as limited as with other options, but it also requires you to work directly with the insurance company | No subsidies, so these plans are usually more expensive than ACA plans or employer plans |

| Medicare | Multiple Medicare Advantage plans are offered by private insurance companies and Original Medicare Most have options with different benefit designs and costs | Must meet age or disability requirements to qualify for Medicare |

| Medicaid | Most affordable option Comprehensive coverage for little to no money Costs based on your income | Must meet the income requirements to qualify Members usually can’t choose between plans You may have trouble finding providers that accept Medicaid in your area |

Most of the time, you can turn down your employer’s group health insurance plan. However, you may have to sign a waiver or prove to your employer that you will get different insurance coverage. If you decide you want to enroll in your employer’s plan at a later time, you can do so during the open enrollment period or if you qualify for a special enrollment period.

Find out more about employer-sponsored health insurance vs. individual plans.